CRR III: The new Capital Requirements Regulation and its impact on the real estate sector

Best Practices & Trends

Published by

PriceHubble

-

Aug 29, 2025

CRR III: The new Capital Requirements Regulation and its impact on the real estate sector

Best Practices & Trends

Published by

PriceHubble

-

Aug 29, 2025

CRR III: The new Capital Requirements Regulation and its impact on the real estate sector

Best Practices & Trends

Published by

PriceHubble

-

Aug 29, 2025

CRR III: Impact of the Capital Requirements Regulation

The Capital Requirements Regulation III (CRR III) entered into force on 1 January 2025, introducing fundamental changes to the calculation of risk-weighted assets (RWA) for banks operating within the European Union. The reform aims to strengthen the resilience of the banking sector and establish a more transparent and risk-sensitive approach to capital requirements, including higher capital buffers and more differentiated risk exposure classes. Real estate finance is particularly affected, with significant implications for both commercial real estate (CRE) and residential real estate (RRE).

This article explains the background and objectives of CRR III, outlines its implications for the real estate sector, and explores how banks can respond effectively to the new regulatory requirements.

What exactly is CRR III?

Often described as the “finalisation of Basel III” or informally as “Basel IV,” CRR III builds on the Basel III framework developed by the Basel Committee on Banking Supervision. Together with amendments introduced through the Capital Requirements Directive VI (CRD VI), the regulation has been refined by the European Banking Authority to incorporate more advanced risk frameworks, including market risk, stress testing methodologies, and loss rate analysis.

Although implementation was delayed due to the pandemic, the European Commission set 1 January 2025 as the effective date following negotiations between the Council of the European Union and the European Parliament and extensive trilogue discussions in 2023.

The objective of CRR III is to enhance the resilience of the European banking system through more transparent and risk-sensitive procedures, supported by internal models and improved reporting requirements. Modern approaches such as the Internal Ratings-Based (IRB) approach are reinforced to strengthen credit-granting processes and regulatory assessments of both individual loans and whole-loan exposures. Compared with CRR II, additional elements such as the Credit Risk Standardised Approach (CRSA) and the Credit Conversion Factor (CCF) are now fully integrated into credit risk and capital requirement calculations. Central banks play a key role in supervising and overseeing implementation.

What does this mean for real estate?

CRR III introduces significant changes for the real estate sector, particularly in the risk weighting of real estate-secured exposures. A clear distinction is made between different types of exposures, including residential and commercial properties where repayments are primarily generated by the property’s cash flow, known as Income Producing Real Estate Exposures (IPRE), and those where this is not the case.

Unsecured IPRE exposures are now assigned a risk weight of 150 percent, reflecting updated technical standards and stricter market risk assessments. This change can substantially increase banks’ risk-weighted assets and, as a result, raise own-funds requirements under the revised prudential framework.

Mortgage exposures and land acquisition, development, and construction (ADC) loans are also affected. These exposures are subject to stricter risk weights, particularly when loan-to-value ratios exceed defined thresholds. Under certain conditions, covered bonds backed by immovable property may benefit from preferential risk weights, offering some relief for lenders specialising in mortgage-backed securities.

The regulation requires banks to conduct detailed analyses of their real estate portfolios and maintain continuous monitoring in line with enhanced reporting obligations and supervisory guidance. Beyond adjusting risk weights, data analysis becomes increasingly critical. By closely tracking market values, revaluation trends, and property-level risk assessments, banks can better manage and potentially optimise the additional capital burden. The integration of ESG risks also plays a growing role in supporting sustainable real estate finance and addressing long-term challenges.

CRR III: Impact of the Capital Requirements Regulation

The Capital Requirements Regulation III (CRR III) entered into force on 1 January 2025, introducing fundamental changes to the calculation of risk-weighted assets (RWA) for banks operating within the European Union. The reform aims to strengthen the resilience of the banking sector and establish a more transparent and risk-sensitive approach to capital requirements, including higher capital buffers and more differentiated risk exposure classes. Real estate finance is particularly affected, with significant implications for both commercial real estate (CRE) and residential real estate (RRE).

This article explains the background and objectives of CRR III, outlines its implications for the real estate sector, and explores how banks can respond effectively to the new regulatory requirements.

What exactly is CRR III?

Often described as the “finalisation of Basel III” or informally as “Basel IV,” CRR III builds on the Basel III framework developed by the Basel Committee on Banking Supervision. Together with amendments introduced through the Capital Requirements Directive VI (CRD VI), the regulation has been refined by the European Banking Authority to incorporate more advanced risk frameworks, including market risk, stress testing methodologies, and loss rate analysis.

Although implementation was delayed due to the pandemic, the European Commission set 1 January 2025 as the effective date following negotiations between the Council of the European Union and the European Parliament and extensive trilogue discussions in 2023.

The objective of CRR III is to enhance the resilience of the European banking system through more transparent and risk-sensitive procedures, supported by internal models and improved reporting requirements. Modern approaches such as the Internal Ratings-Based (IRB) approach are reinforced to strengthen credit-granting processes and regulatory assessments of both individual loans and whole-loan exposures. Compared with CRR II, additional elements such as the Credit Risk Standardised Approach (CRSA) and the Credit Conversion Factor (CCF) are now fully integrated into credit risk and capital requirement calculations. Central banks play a key role in supervising and overseeing implementation.

What does this mean for real estate?

CRR III introduces significant changes for the real estate sector, particularly in the risk weighting of real estate-secured exposures. A clear distinction is made between different types of exposures, including residential and commercial properties where repayments are primarily generated by the property’s cash flow, known as Income Producing Real Estate Exposures (IPRE), and those where this is not the case.

Unsecured IPRE exposures are now assigned a risk weight of 150 percent, reflecting updated technical standards and stricter market risk assessments. This change can substantially increase banks’ risk-weighted assets and, as a result, raise own-funds requirements under the revised prudential framework.

Mortgage exposures and land acquisition, development, and construction (ADC) loans are also affected. These exposures are subject to stricter risk weights, particularly when loan-to-value ratios exceed defined thresholds. Under certain conditions, covered bonds backed by immovable property may benefit from preferential risk weights, offering some relief for lenders specialising in mortgage-backed securities.

The regulation requires banks to conduct detailed analyses of their real estate portfolios and maintain continuous monitoring in line with enhanced reporting obligations and supervisory guidance. Beyond adjusting risk weights, data analysis becomes increasingly critical. By closely tracking market values, revaluation trends, and property-level risk assessments, banks can better manage and potentially optimise the additional capital burden. The integration of ESG risks also plays a growing role in supporting sustainable real estate finance and addressing long-term challenges.

CRR III: Impact of the Capital Requirements Regulation

The Capital Requirements Regulation III (CRR III) entered into force on 1 January 2025, introducing fundamental changes to the calculation of risk-weighted assets (RWA) for banks operating within the European Union. The reform aims to strengthen the resilience of the banking sector and establish a more transparent and risk-sensitive approach to capital requirements, including higher capital buffers and more differentiated risk exposure classes. Real estate finance is particularly affected, with significant implications for both commercial real estate (CRE) and residential real estate (RRE).

This article explains the background and objectives of CRR III, outlines its implications for the real estate sector, and explores how banks can respond effectively to the new regulatory requirements.

What exactly is CRR III?

Often described as the “finalisation of Basel III” or informally as “Basel IV,” CRR III builds on the Basel III framework developed by the Basel Committee on Banking Supervision. Together with amendments introduced through the Capital Requirements Directive VI (CRD VI), the regulation has been refined by the European Banking Authority to incorporate more advanced risk frameworks, including market risk, stress testing methodologies, and loss rate analysis.

Although implementation was delayed due to the pandemic, the European Commission set 1 January 2025 as the effective date following negotiations between the Council of the European Union and the European Parliament and extensive trilogue discussions in 2023.

The objective of CRR III is to enhance the resilience of the European banking system through more transparent and risk-sensitive procedures, supported by internal models and improved reporting requirements. Modern approaches such as the Internal Ratings-Based (IRB) approach are reinforced to strengthen credit-granting processes and regulatory assessments of both individual loans and whole-loan exposures. Compared with CRR II, additional elements such as the Credit Risk Standardised Approach (CRSA) and the Credit Conversion Factor (CCF) are now fully integrated into credit risk and capital requirement calculations. Central banks play a key role in supervising and overseeing implementation.

What does this mean for real estate?

CRR III introduces significant changes for the real estate sector, particularly in the risk weighting of real estate-secured exposures. A clear distinction is made between different types of exposures, including residential and commercial properties where repayments are primarily generated by the property’s cash flow, known as Income Producing Real Estate Exposures (IPRE), and those where this is not the case.

Unsecured IPRE exposures are now assigned a risk weight of 150 percent, reflecting updated technical standards and stricter market risk assessments. This change can substantially increase banks’ risk-weighted assets and, as a result, raise own-funds requirements under the revised prudential framework.

Mortgage exposures and land acquisition, development, and construction (ADC) loans are also affected. These exposures are subject to stricter risk weights, particularly when loan-to-value ratios exceed defined thresholds. Under certain conditions, covered bonds backed by immovable property may benefit from preferential risk weights, offering some relief for lenders specialising in mortgage-backed securities.

The regulation requires banks to conduct detailed analyses of their real estate portfolios and maintain continuous monitoring in line with enhanced reporting obligations and supervisory guidance. Beyond adjusting risk weights, data analysis becomes increasingly critical. By closely tracking market values, revaluation trends, and property-level risk assessments, banks can better manage and potentially optimise the additional capital burden. The integration of ESG risks also plays a growing role in supporting sustainable real estate finance and addressing long-term challenges.

Impact on different banking models

The impact of CRR III varies significantly depending on a bank’s business model. Large, internationally active banks using complex internal models under the Internal Ratings-Based Approach face particular challenges related to the Output Floor, which establishes a minimum level of capital requirements. This can lead to materially higher capital buffers and may require substantial adjustments to risk models and loan portfolios.

Smaller banks and institutions focused on SME lending and applying the standardised approach are generally less affected. In particular, the SME supporting factor helps limit the regulatory burden for these banks. Overall, the consequences of CRR III depend heavily on institutional size, geographic scope, and lending focus.

How can banks implement CRR III requirements?

Since CRR III became effective on 1 January 2025, banks have been required to implement the new framework across capital, liquidity, and credit risk methodologies. This includes addressing derivatives exposure, market risk assessments, and internal ratings-based models while adapting to evolving trends in financial services. To manage higher capital requirements and ensure regulatory alignment, banks should consider the following measures:

Data analysis and portfolio monitoring

By using advanced analytics, banks can monitor property values in real time, run scenario analyses, and respond quickly to market changes. This is particularly important for calculating additional capital requirements for unsecured IPRE exposures and managing off-balance-sheet risks. Continuous asset revaluation supports more accurate capital planning and regulatory compliance.

ESG integration

Sustainability considerations are increasingly central to property valuation. Integrating ESG data into valuation and risk models helps banks meet CRR III requirements while promoting sustainable real estate financing.

Risk modelling

Detailed risk models allow banks to clearly assess the impact of new risk weights on capital ratios. This transparency supports strategic adjustments to offset higher capital requirements while maintaining competitiveness. Transitional arrangements, enhanced reporting, and improved operational risk analysis further support implementation.

Other regulatory adjustments

Pilot projects and targeted implementation initiatives can help institutions manage loan exposures more effectively and classify risk categories accurately. Ongoing portfolio reassessment, including comparisons between whole-loan and loan-splitting approaches, remains an essential component.

By proactively adopting these measures, banks can meet CRR III’s regulatory demands, strengthen their market position, and support a sustainable long-term business model.

Practical challenges in implementation

Beyond conceptual changes, CRR III introduces significant practical challenges. Banks must upgrade IT systems and data management frameworks to handle increased data granularity and new risk modelling requirements. This often involves extensive system changes, additional data sources, and enhanced validation processes.

Comprehensive staff training is also essential, as departments including risk management, controlling, IT, and compliance must realign their processes. Coordination with external regulators adds further complexity. Addressing these challenges requires sustained investment, strategic realignment, and ongoing operational adaptation.

Impact on different banking models

The impact of CRR III varies significantly depending on a bank’s business model. Large, internationally active banks using complex internal models under the Internal Ratings-Based Approach face particular challenges related to the Output Floor, which establishes a minimum level of capital requirements. This can lead to materially higher capital buffers and may require substantial adjustments to risk models and loan portfolios.

Smaller banks and institutions focused on SME lending and applying the standardised approach are generally less affected. In particular, the SME supporting factor helps limit the regulatory burden for these banks. Overall, the consequences of CRR III depend heavily on institutional size, geographic scope, and lending focus.

How can banks implement CRR III requirements?

Since CRR III became effective on 1 January 2025, banks have been required to implement the new framework across capital, liquidity, and credit risk methodologies. This includes addressing derivatives exposure, market risk assessments, and internal ratings-based models while adapting to evolving trends in financial services. To manage higher capital requirements and ensure regulatory alignment, banks should consider the following measures:

Data analysis and portfolio monitoring

By using advanced analytics, banks can monitor property values in real time, run scenario analyses, and respond quickly to market changes. This is particularly important for calculating additional capital requirements for unsecured IPRE exposures and managing off-balance-sheet risks. Continuous asset revaluation supports more accurate capital planning and regulatory compliance.

ESG integration

Sustainability considerations are increasingly central to property valuation. Integrating ESG data into valuation and risk models helps banks meet CRR III requirements while promoting sustainable real estate financing.

Risk modelling

Detailed risk models allow banks to clearly assess the impact of new risk weights on capital ratios. This transparency supports strategic adjustments to offset higher capital requirements while maintaining competitiveness. Transitional arrangements, enhanced reporting, and improved operational risk analysis further support implementation.

Other regulatory adjustments

Pilot projects and targeted implementation initiatives can help institutions manage loan exposures more effectively and classify risk categories accurately. Ongoing portfolio reassessment, including comparisons between whole-loan and loan-splitting approaches, remains an essential component.

By proactively adopting these measures, banks can meet CRR III’s regulatory demands, strengthen their market position, and support a sustainable long-term business model.

Practical challenges in implementation

Beyond conceptual changes, CRR III introduces significant practical challenges. Banks must upgrade IT systems and data management frameworks to handle increased data granularity and new risk modelling requirements. This often involves extensive system changes, additional data sources, and enhanced validation processes.

Comprehensive staff training is also essential, as departments including risk management, controlling, IT, and compliance must realign their processes. Coordination with external regulators adds further complexity. Addressing these challenges requires sustained investment, strategic realignment, and ongoing operational adaptation.

Impact on different banking models

The impact of CRR III varies significantly depending on a bank’s business model. Large, internationally active banks using complex internal models under the Internal Ratings-Based Approach face particular challenges related to the Output Floor, which establishes a minimum level of capital requirements. This can lead to materially higher capital buffers and may require substantial adjustments to risk models and loan portfolios.

Smaller banks and institutions focused on SME lending and applying the standardised approach are generally less affected. In particular, the SME supporting factor helps limit the regulatory burden for these banks. Overall, the consequences of CRR III depend heavily on institutional size, geographic scope, and lending focus.

How can banks implement CRR III requirements?

Since CRR III became effective on 1 January 2025, banks have been required to implement the new framework across capital, liquidity, and credit risk methodologies. This includes addressing derivatives exposure, market risk assessments, and internal ratings-based models while adapting to evolving trends in financial services. To manage higher capital requirements and ensure regulatory alignment, banks should consider the following measures:

Data analysis and portfolio monitoring

By using advanced analytics, banks can monitor property values in real time, run scenario analyses, and respond quickly to market changes. This is particularly important for calculating additional capital requirements for unsecured IPRE exposures and managing off-balance-sheet risks. Continuous asset revaluation supports more accurate capital planning and regulatory compliance.

ESG integration

Sustainability considerations are increasingly central to property valuation. Integrating ESG data into valuation and risk models helps banks meet CRR III requirements while promoting sustainable real estate financing.

Risk modelling

Detailed risk models allow banks to clearly assess the impact of new risk weights on capital ratios. This transparency supports strategic adjustments to offset higher capital requirements while maintaining competitiveness. Transitional arrangements, enhanced reporting, and improved operational risk analysis further support implementation.

Other regulatory adjustments

Pilot projects and targeted implementation initiatives can help institutions manage loan exposures more effectively and classify risk categories accurately. Ongoing portfolio reassessment, including comparisons between whole-loan and loan-splitting approaches, remains an essential component.

By proactively adopting these measures, banks can meet CRR III’s regulatory demands, strengthen their market position, and support a sustainable long-term business model.

Practical challenges in implementation

Beyond conceptual changes, CRR III introduces significant practical challenges. Banks must upgrade IT systems and data management frameworks to handle increased data granularity and new risk modelling requirements. This often involves extensive system changes, additional data sources, and enhanced validation processes.

Comprehensive staff training is also essential, as departments including risk management, controlling, IT, and compliance must realign their processes. Coordination with external regulators adds further complexity. Addressing these challenges requires sustained investment, strategic realignment, and ongoing operational adaptation.

Innovative solutions to meet CRR III

CRR III marks a critical step in strengthening the stability of Europe’s banking sector. In real estate finance, the new framework leads to materially higher capital requirements, particularly for unsecured IPRE exposures. Banks must reassess their portfolios through detailed data analysis and continuous monitoring.

By leveraging innovative solutions, integrated ESG data, and optimised risk models, banks can navigate these regulatory complexities more effectively. Advanced real estate valuation and risk management tools enable institutions to manage capital requirements efficiently while remaining compliant with evolving prudential standards and borrower risk profiles.

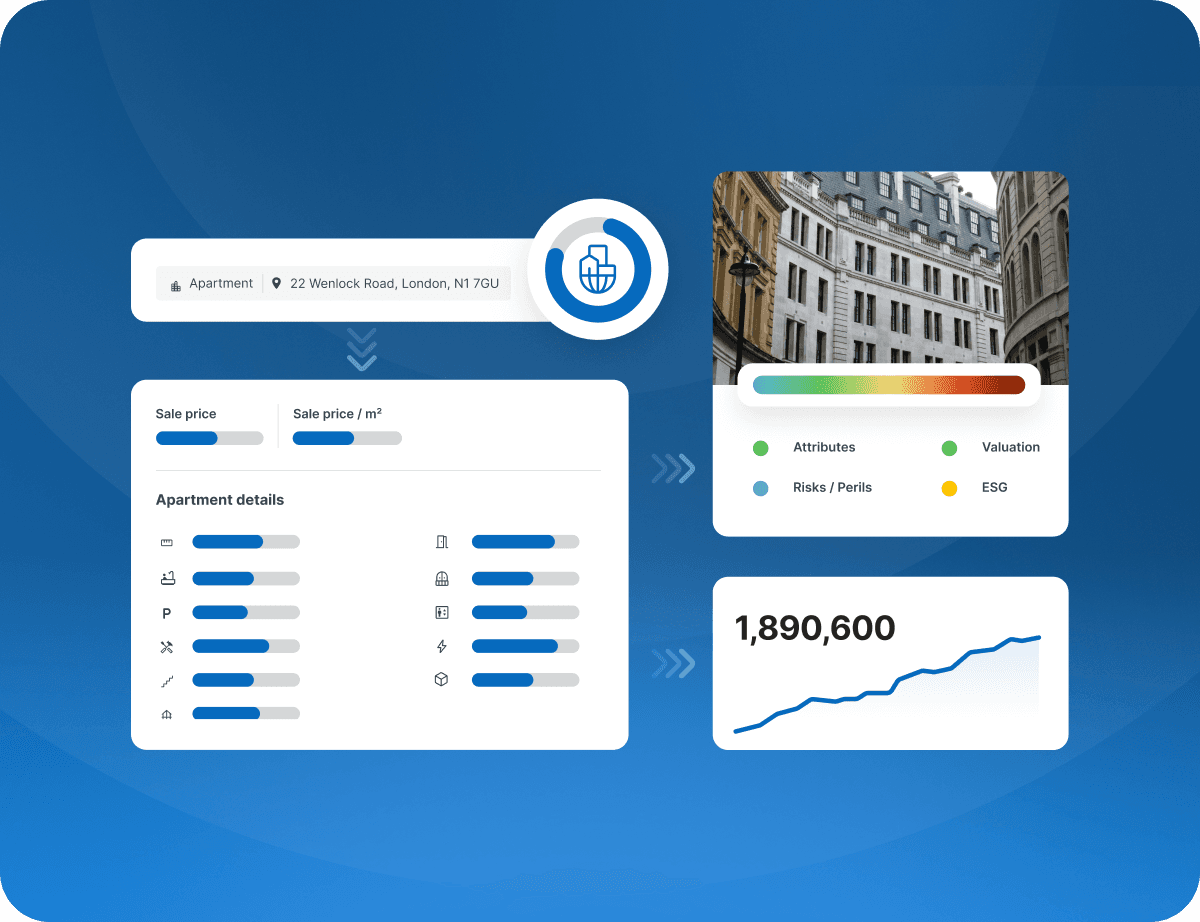

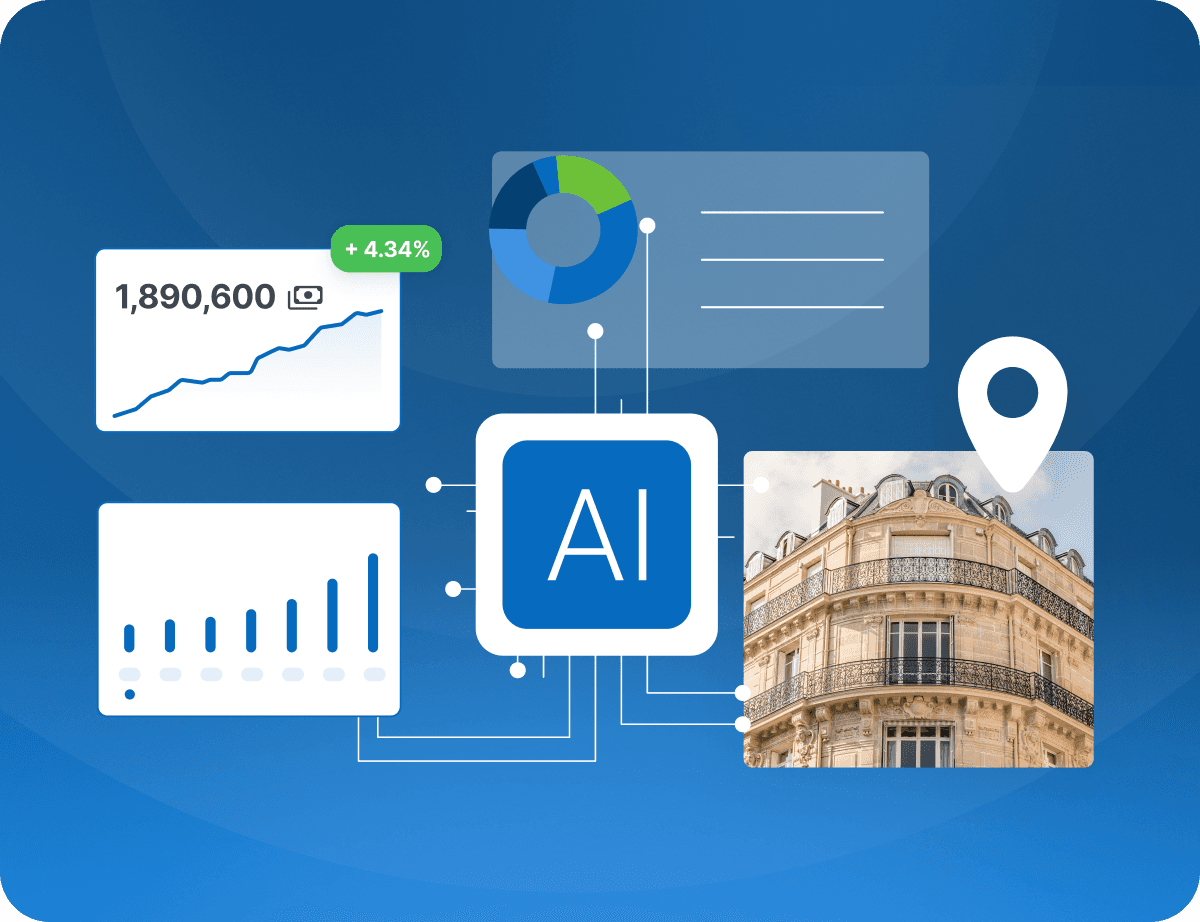

PriceHubble’s AI-driven property performance systems support accurate valuation and monitoring of real estate portfolios. By capturing and analysing CRR III-relevant metrics such as risk weights, the platform enables real-time monitoring and scenario analysis. The integration of ESG data into valuation models further supports regulatory compliance and sustainable financing. Detailed risk modelling helps banks transparently assess the impact of new risk weights on capital ratios and adjust strategies accordingly.

With PriceHubble’s property performance systems, banks can optimise their real estate portfolios to meet CRR III requirements. Book a demo with our team and discover how.

Innovative solutions to meet CRR III

CRR III marks a critical step in strengthening the stability of Europe’s banking sector. In real estate finance, the new framework leads to materially higher capital requirements, particularly for unsecured IPRE exposures. Banks must reassess their portfolios through detailed data analysis and continuous monitoring.

By leveraging innovative solutions, integrated ESG data, and optimised risk models, banks can navigate these regulatory complexities more effectively. Advanced real estate valuation and risk management tools enable institutions to manage capital requirements efficiently while remaining compliant with evolving prudential standards and borrower risk profiles.

PriceHubble’s AI-driven property performance systems support accurate valuation and monitoring of real estate portfolios. By capturing and analysing CRR III-relevant metrics such as risk weights, the platform enables real-time monitoring and scenario analysis. The integration of ESG data into valuation models further supports regulatory compliance and sustainable financing. Detailed risk modelling helps banks transparently assess the impact of new risk weights on capital ratios and adjust strategies accordingly.

With PriceHubble’s property performance systems, banks can optimise their real estate portfolios to meet CRR III requirements. Book a demo with our team and discover how.

Innovative solutions to meet CRR III

CRR III marks a critical step in strengthening the stability of Europe’s banking sector. In real estate finance, the new framework leads to materially higher capital requirements, particularly for unsecured IPRE exposures. Banks must reassess their portfolios through detailed data analysis and continuous monitoring.

By leveraging innovative solutions, integrated ESG data, and optimised risk models, banks can navigate these regulatory complexities more effectively. Advanced real estate valuation and risk management tools enable institutions to manage capital requirements efficiently while remaining compliant with evolving prudential standards and borrower risk profiles.

PriceHubble’s AI-driven property performance systems support accurate valuation and monitoring of real estate portfolios. By capturing and analysing CRR III-relevant metrics such as risk weights, the platform enables real-time monitoring and scenario analysis. The integration of ESG data into valuation models further supports regulatory compliance and sustainable financing. Detailed risk modelling helps banks transparently assess the impact of new risk weights on capital ratios and adjust strategies accordingly.

With PriceHubble’s property performance systems, banks can optimise their real estate portfolios to meet CRR III requirements. Book a demo with our team and discover how.

See also

News

Read more →

News

Read more →

News

Read more →

Request a demo

We will get back to you quickly.

We look forward to speaking with you.

Thank you!

We will get back to you within 24 business hours.

Thank you!

We will get back to you within 24 business hours.