Let’s take a closer look at the ways in which an increased use of AVM based solutions can be beneficial for banks and financial institutions:

Assessment and valuation of guarantees and collateral through AVMs

By opening up the process to AI based models, the EBA aims to operationalise collateral valuation in the credit process. This not only creates greater transparency, but grants banks access to up-to-date information on the properties they are financing at all times. For that purpose, the performance of statistical models has taken an enormous leap forward in recent years.

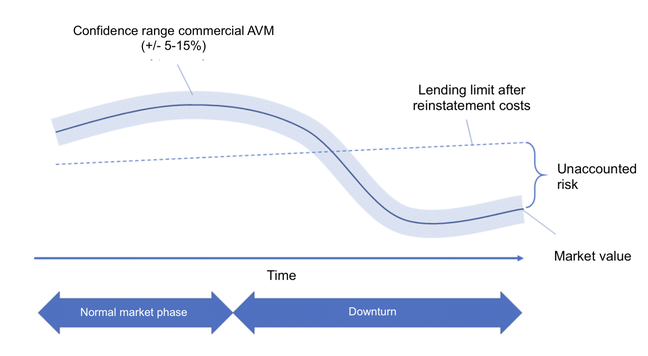

AVMs are now able to determine the statistically most probable market and rental price for any residential property at any location on the basis of available data, taking into account not only traditional characteristics, but also less common criteria and metrics which have a proven impact on the price, such as noise pollution, socio-demographics, accessibility, or even construction projects in the surrounding area. AVMs also capture complex relationships that cannot be accounted for in traditional valuation, and make it possible to determine market value with a valuation accuracy of 5 to 15 percent deviation.

In other countries, such as Switzerland, semi-automated processes have already become more common through the use of hedonic models. It is possible, with the help of digital authentication, to carry out the extension of a mortgage completely digitally without an advisor.

Risk management: an opportunity to get closer to the market

In the risk management department of many European banks, such AVMs are still completely underrepresented today, despite the fact that they offer many advantages.

As an example, in Germany, a conservative price determination such as the asset value method according to the Real Estate Value Determination Ordinance (“ImmoWertV”) takes into account the standard land value and the production costs of the property and are, if necessary, corrected by applying a market adjustment factor.

However, this procedure doesn’t accurately take into account, for example, economic changes at the location resulting from migration, or the increase in construction costs. As a result, the production costs considered in the valuation at the time of the loan no longer correspond to the actual production costs and thus, to the market price.

Since an AVM is able to reflect such changes in real time, it is then even much more conservative in its valuation. If such changes in the market do not flow into the valuation at the time of lending and also not into the ongoing credit monitoring of existing loans, the bank takes easily avoidable risks. On the contrary, if the valuation is too conservative compared to the actual market price, banks may miss out on business by failing to recognise the value of the property and rejecting a worthwhile loan transaction.

The use of AVMs can thus support credit institutions in the form of a pre-due diligence already in the first step of the consumer credit life cycle.